No ifs and buts, the Q2 GDP print shows pain all around for Malaysia’s economy during the period. At -17.1% yoy, the slump is the sharpest ever and came much worse than what we and the market had expected too. In qoq sa terms, the sequential growth of -11.4% after -2% in Q1 is also an arithmetic tally of what we already know – the economy had a recession.

Details show multiple hits on multiple sectors. The crucial private consumption slumped by 18.5% yoy, as consumers pulled back despite cash handouts and a blanket loans moratorium. Investment and exports shrank even more sharply; victims of poor outlook and production shutdown alike during the MCO period. Only government spending proved supportive.

As nasty as the numbers were, there are silver linings to be seen, however. For one, intra-quarter, while April and May contractions were deep, most activities have rebounded encouragingly by June and beyond – signalling to us that the worst is over. While the MCO in Malaysia compounded the economic damage in Q2, the payoff is clear now: Malaysia has gotten its pandemic situation under control – and that will aid the economy to regain its footing.

Damage Assessment

Today’s Q2 GDP data release for Malaysia shows the scale of the destruction that the pandemic has brought to the economy over the period. At a growth rate of -17.1% yoy, the data shows that the deepest contraction in any quarter, even worse than the -11.2% that Malaysia went through in Q4 1998 at the height of the Asian Financial Crisis.

In seasonally adjusted terms, the economy shrank by 16.5% from the previous quarter, following a 2% sequential contraction in Q1, and hence ‘qualifying’ for the common morbid threshold of a technical recession.

Looking at the expenditure component details, it is clear that the bulk of the pain came from a sharp pullback in household consumption and investment activities.

To begin with, now that the bulk of Malaysia’s economy comprises of private consumption – it commanded a hefty 61.7% of GDP previously in Q1 – whatever happens there would naturally have an important bearing on the economy.

Before the GDP data release, we had fairly high hopes that the relative strength of consumption that we saw in Q1 could put it in a better stead to withstand the onslaught of the challenges in Q2. Moreover, we had anticipated better pass-through from the rounds of stimulus handouts by the government, as well as the positive net effect of loans moratorium – in which individuals were offered blanket suspension of loans servicing for half a year – to at least cushion the blow more robustly.

Alas, as it turns out, it appears that the more dramatic effects of being locked down at home for nearly two months during the MCO as well as the cloud of unemployment rate ticking up to 5.3% in May (before coming down to 4.9% in June) appear to have the much larger effect.

Private consumption shrank by a massive 18.5% yoy, and shaved off headline GDP growth by a hefty 10.7 percentage points (ppt) over the period, instead of a much milder 4-6ppt that we had pencilled in.

The other ‘contributor’ to the deep negative headline GDP growth print is the exports sector, which grew by -21.7%yoy and cut overall growth down by nearly 14ppt. Given the production shutdown during the MCO period, coupled with the deep global demand slump, the pullback in exports does not come as a surprise. If anything, as we mentioned before in a previous report, by June, we already started to see this segment recovering rather sharply – with a surprise positive growth rather than a contraction as expected.

In net trade terms, the damage was blunted by a rather sharp decrease in import activities as well. Indeed, the shrinking of imports – due to pullback in demand from Malaysian consumers and businesses alike – contributed a net positive 11.3ppt to headline growth.

Elsewhere, investment activities shrank by nearly 29% yoy, negating headline growth by over 7ppt, as businesses pulled back from any major investment undertaking understandably during a period of massive uncertainties. Meanwhile, government consumption grew by 2.3% yoy. Although it added just a minuscule 0.26ppt to headline growth, the very fact that it is a positive contributor is laudable, as disbursing stimulus money is not as easy as it seems, as other countries including Indonesia has been finding out.

Road to Recovery

As painful as the multiple hits were throughout the data, however, there are silver linings to look out for. Indeed, if we can – literally – borrow a page from its press release which accompanies today’s GDP data announcement, Bank Negara Malaysia (BNM) has rightly pointed out the multiple V-shaped uptick in a number of key indicators.

Indeed, as signalled by the charts above, even though April and May saw deep contractions across major economic indicators ranging from trade and industrial production to credit card spending and electricity generation, there has also been a sharp recovery starting from June, akin to the uptick in export activities that we mentioned earlier.

To be sure, the Q2 pain might have been sharper than expected and, in and of its own, would pull down our 2020 growth forecast from -2.6% to now -5.1% yoy, our baseline expectation is for a fairly steady sequential uptick from here. We see GDP growth coming in still negative in Q3, but at a milder -4% yoy growth before reaching 0% in Q4. For their part, BNM is now expecting the 2020 growth to be within the range of -3.5% to -5.5%, compared to -2% to 0.5% before.

When it comes to policy reactions, we continue to see a good chance of BNM cutting rate further by 25bps to a new record-low of 1.5% when the MPC meets next on September 10th. Even though BNM gives off an optimistic vibe in its H2 outlook, signalling that recovery is already taking place, we see that, on balance, the sharp magnitude of Q2’s GDP hit and the still-uncertain global outlook in H2 would warrant another ‘insurance cut’ akin to its action in the July MPC meeting.

Moreover, the timing of the cut would be propitious, as well, as it comes not long before the expiration of the 6-month loans moratorium. Even though the authorities have extended the moratorium for some categories of borrowers – those who have unfortunately lost their jobs – and allowed for proportionally reduced payment – for those who saw their pays cut – the moratorium is no longer enacted in blanket terms across the board for all borrowers.

Given that the moratorium has been a key factor in supporting private consumption – which would have slumped even more considerably in Q2 without it – the need to ease the sudden transition back towards having to service their loans once more for the consumers has become even more apparent.

Hence, continuing to help the majority of borrowers amid a still-uncertain environment, easing interest rate burden via another OPR cut could be one factor of consideration by the MPC, especially when inflation outlook remains tame, with BNM still keeping to the projected range of -1.5% to 0.5% for this year.

It is telling for instance that a recent survey by Property Guru Malaysia, a property listing portal, for example, showed that as many as 81% of respondents cite reduction of home loan interest rates as part of initiatives that they would like to see from the authorities. The same survey indicates that among all the stimulus efforts thus far, they are most satisfied with the BNM’s 6-month loans moratorium. Now that the latter measure is slated to end soon, there might be more onus on seeing more of the former in terms of easing interest rates.

Moreover, apart from the more traditional way of easing policy rate further, BNM may have hinted at the potential for other, more unconventional measures today. As quoted by Bloomberg, BNM’s Governor Nor Shamsiah Mohd Yunus said that “Should there be a second outbreak, there is room for targeted policy measures to complement the ones implemented earlier. For example, the bank’s policy levers can be expanded or extended within this mandate.”

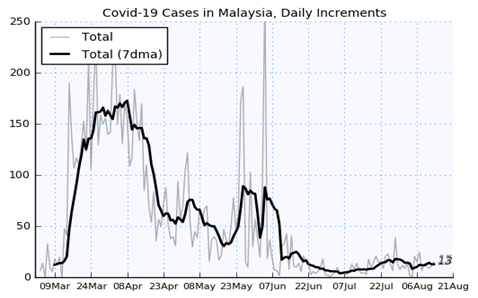

Although Malaysia’s early-and-decisive MCO restriction orders have managed to keep new coronavirus cases under control – with new infections at low teens compared to more than 200 in late March – judging from the experience in other countries, there is always the risk of a sudden resurgence. In that case, touch wood, there might well be a scenario of secondary lockdowns that would bring the economic recovery to a halt again. This could then prompt the government to have to step in again with further fiscal stimulus that would push up fiscal deficit from 6% of GDP that is anticipated this year.

Already, even at the current rate, debt-to-GDP ratio is already slated to be north of the 55% threshold that is necessitating a legislative approval discussed in the parliament now. If there is indeed a need for further forceful fiscal action, either due to domestic lockdown or another massive global slowdown, the resultant uptick in debt supply might well necessitate more active involvement by the central bank.

It is perhaps that very spirit of scenario-planning that prompted the governor’s comment in terms of highlighting the potential ‘expansion’ and ‘extension’ of its toolkits. To us, again in the spirit of thinking of different scenarios rather than hashing out the baseline expectation, it is not inconceivable for BNM to start joining its peers such as Bank Indonesia and, more recently, Bangko Sentral ng Pilipinas, in actively purchasing government debts at a time when increased government bond supply might not be met with increased market demand, even if so far, the MGS market appears to be well-bid by market players.

While outright sovereign debt purchase by BNM outside of the usual monetary policy operations is, again, not within our current baseline expectation, the presence of a multitude of potential bugbears on the global front at a time when virus resurgence is an evident danger in many countries, perhaps we should remember the adage of never say never.

Written by: Wellian Wiranto, Economist, Global Treasury – Research & Strategy, OCBC Bank

Read more: Should we be stressed about the lack of market stress?

Discussion about this post