UK CAR AND COMMERCIAL VEHICLE MANUFACTURING (data for December and FY 2025)

Hi-res charts available via Dropbox: https://www.dropbox.com/scl/fo/8pskgvu0pspx9u6ueezx7/ADFoByA30j35QgD6fuNPlXE?rlkey=4yq5xdkri6rdzppkgh1eqlmte&st=o1ruv9dj&dl=0

- Vehicle production down -15.5% in 2025 as 764,715 cars and commercial vehicles leave factories.

- Car output falls -8.0% while CV volumes decline -62.3% as industry restructures amid cyber incident and tariff uncertainties.

- December car growth signals optimism for 2026, driven by new EV models entering production, with opportunity to produce one million vehicles by 2027 if conditions are right.

- Sector calls for government to deliver Industrial and Trade Strategies, to improve manufacturing competitiveness and unlock growth potential.

LONDON, Jan. 29, 2026 /PRNewswire/ — UK vehicle production fell -15.5% in 2025, according to the latest figures published today by the Society of Motor Manufacturers and Traders (SMMT). Factories turned out a total of 764,715 units – 717,371 cars and 47,344 commercial vehicles, with output falling by -8.0% and -62.3% respectively.1 Volumes were constrained by a number of factors, including a cyber incident stopping production at Britain’s biggest automotive employer; new tariffs on trade across the Atlantic; the consolidation of two CV plants into one; and ongoing restructuring as plants shift to a decarbonised future.

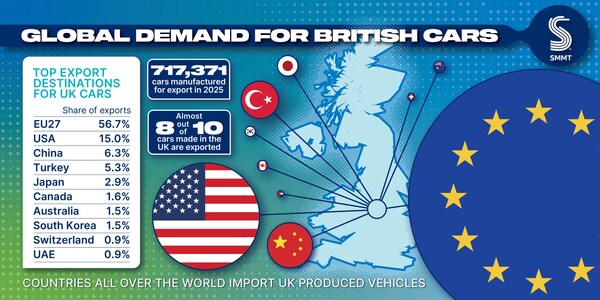

UK global car exports 2025

December saw van, truck, bus and coach volumes decline for a ninth consecutive month, falling -67.7% to 2,281 units, but car production showed signs of recovery, rising 17.7% to 53,003 units and ending four months of decline. Over the year, car production for the UK market fell by -8.2% to 161,545 units while exports declined -7.9% to 555,826 units, accounting for 77.5% of output.

Europe received the majority (56.7%) of vehicles exported, followed by the US (15.0%) and China (6.3%). Exports to each were down, by -3.3%, -18.3% and -12.5% respectively – with shipments to the US impacted by tariff uncertainty earlier in 2025. Turkey and Japan rounded off the UK’s top five global export markets, followed by Canada, Australia, South Korea, Switzerland and UAE.

Production of battery electric (BEV), plug-in hybrid (PHEV) and hybrid (HEV) cars rose by 8.3% to a combined 298,813 units – a record 41.7% share of output. With the start of next generation volume electric car production in Sunderland, and the planned launch of seven new EV models across the UK, output is expected to grow in 2026.

The latest independent production outlook expects overall UK car production to return to growth with output set to rise by more than 10% to some 790,000 units in 2026. Overall light vehicle production is anticipated to reach 824,000 units – with the potential to reach one million units by 2027 provided new model launches stay on track and the right conditions are set.2

Significant public and private investment has already been committed to the UK’s EV transition –with government’s £4 billion DRIVE35 programme launched as part of its Modern Industrial Strategy. Achieving the Strategy’s ambition of UK automotive production reaching over 1.3 million per year by 2035 now depends on the delivery of the commitments set out in the Strategy.

These include measures to drive down the UK’s stubbornly high cost of energy, ensuring the whole sector is eligible for the British Industrial Competitiveness Scheme, support for the UK supply chain, and the creation of a strong and sustainable domestic market. Given that manufacturers – and therefore suppliers – build close to where they sell, the importance of a healthy new vehicle market cannot be overstated.

A forward-looking trade agenda that deepens existing relationships and builds new ones is also fundamental to what is an export-led industry. Europe remains the UK’s biggest automotive export market and the biggest source of imported vehicles and components, so tariff-free trade and market access must be assured, despite a looming change to Rules of Origin requirements agreed under the Brexit deal and increasingly protectionist ‘Made in Europe’ proposals coming from the European Commission.

Furthermore, given the crucial role of US exports – especially to small volume, high value manufacturers – further uncertainty in cross-Atlantic trade has to be avoided while the benefits arising from new deals with South Korea and India must be realised. Above all, the UK must continue to promote the sector’s expertise and capability vigorously to a global audience.

Mike Hawes, SMMT Chief Executive, said, “2025 was the toughest year in a generation for UK vehicle manufacturing. Structural changes, new trade barriers, and a cyber attack that stopped production at one of the UK’s most important manufacturers combined to constrain output, but the outlook for 2026 is one of recovery. The launch of a raft of new, increasingly electric, models and an improving economic outlook in key markets augur well. The key to long term growth, however, is the creation of the right competitive conditions for investment; reduced energy costs; the avoidance of new trade barriers; and a healthy, sustainable domestic market. Government has set out how it will back the sector with its Industrial and Trade strategies, and 2026 must be a year of delivery.”

Notes to editors

1 – ‘Commercial vehicle’ covers vans, trucks, taxis, buses and coaches.

2 – Based on independent production outlook produced by AutoAnalysis in November – cars and light vans only.

{kind=link}